Building up sufficient amounts of cash for key life events such as retirement, a house deposit or wedding is a necessity for most people. But here in the UK millions could be looking at a bleak financial future given the low amounts that households are currently saving.

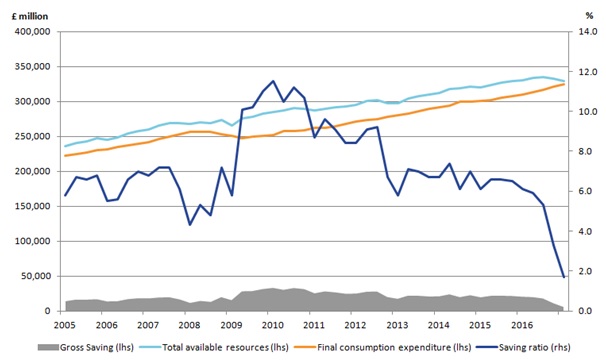

Recent data from the Office for National Statistics showed that in the first three months of 2017 the amount being set aside by households as savings fell to just 1.7% of disposable income (see chart below – dark blue line). This is the lowest level on record and well below the c.10% average seen over the last 50 years.

UK final consumption expenditure, total available resources, gross saving and saving ratio, seasonally adjusted. UK, Quarter 1 (Jan to Mar) 2005 to Quarter 1 2017

Source: Office for National Statistics

But there are further issues, as highlighted by a recent report by independent economic and social policy think tank The Social Market Foundation named Saving Better.

The body notes a wider problem with the behaviour of those people who actually do choose to save some of their income. In short, the main problem is that they are not making the most of their money given a strong bias for holding very low risk and easily accessible asset classes. These include current accounts, cash savings accounts and cash ISAs, which in many cases account for a large proportion of an individual’s total savings.

While it is completely understandable that savers can have a risk averse attitude, the hard fact is that they are losing out on the potential to make higher returns and increase their wealth.

Saving Better suggests that there is around £200 billion in “excess” cash savings in the UK (excess defined as being more than needed to cover “rainy day” needs). If that money had instead been invested in the FTSE 100 over the past five years UK savers would have earned an additional £94 billion, or a 47% return.

Not only that, with interest rates currently at an all time low and inflation standing at 2.6%, most cash investors are seeing the real value of their savings fall month on month.

Saving Better finds that money left in instant access cash savings accounts would have fallen in value by over 4% in real terms over the last five years due to inflation. That a loss of £8 billion on the excess £200 billion. And it’s not only themselves that they could be hurting, with the lack of diversification potentially starving start-up and growth businesses from much needed expansion capital.

But there is a way for savers to help both themselves and smaller companies seeking finance.

Launched by the government in April 2016 is the Innovative Finance ISA (also known as the IF-ISA). It enables investors to earn a tax free* return on loans and bonds issued by peer-to-peer (P2P) lenders and crowdfunding companies by putting them within the ISA wrapper. These typically take the form of business loans, whereby investors lend their money to companies looking for growth capital.

The main attraction of these financial assets, such as the “crowd bonds” offered by Crowd for Angels, is that the interest rates on offer are higher than on Cash ISAs, balanced by higher risks associated with lending to companies.

To give one example of a crowd bond, telecoms business Phenomenon One Communications, is currently looking for investors through Crowd for Angels. The company is seeking up to £250,000 by issuing a crowd bond and in return is offering interest of 8% p.a., paid monthly, fixed for one year. The minimum investment is £100.

For more information on crowd bonds and Phenomenon One CLICK HERE

RISK WARNING

Investing in debt pitches through Crowd for Angels (UK) Limited involves lending to companies and therefore your capital is at risk and interest payments are not guaranteed if the borrower defaultsThe availability of any tax relief depends on the individual circumstances of each investor and of the company concerned, and may be subject to change in the future.

Please click here to read the full Risk Warning.